Menu

As outlined in our recent post, 2024 Estate and Gift Tax Update, the current federal estate tax exemption is the highest level it has ever been (other than 2010 and before there was an estate tax). The unified exemption limit for individuals dying in 2024 is $13,610,000.00 per individual or $27,220,000 for a married couple. Estates are taxed at the rate of 40% for every dollar over the exemption limit. Keep in mind, that this also takes into account any taxable gifts made during the decedent’s lifetime (Video: Gift Tax Exclusion: How much can you give per year?).

As outlined in our recent post, 2024 Estate and Gift Tax Update, the current federal estate tax exemption is the highest level it has ever been (other than 2010 and before there was an estate tax). The unified exemption limit for individuals dying in 2024 is $13,610,000.00 per individual or $27,220,000 for a married couple. Estates are taxed at the rate of 40% for every dollar over the exemption limit. Keep in mind, that this also takes into account any taxable gifts made during the decedent’s lifetime (Video: Gift Tax Exclusion: How much can you give per year?).

While the current federal estate and gift tax exemption is historically high, and it does leave most farms in a position where federal estate taxes are not a current concern, this exemption is scheduled to sunset in the year 2026. At that time, the exemption amount is projected to be $6,980,000.00, or $13,960,000.00 for a married couple. This means that farm operations that continue to be held in the hands of the older generation are more at risk – in some cases, substantially more.

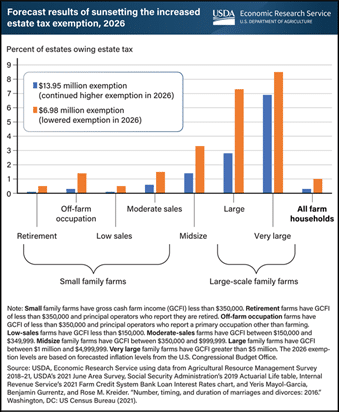

Researchers with the UDSA, Economic Research Service (ERS) estimated that the decreased exemption in 2026 would increase the percent of farm operator estates taxed from 0.3 to 1.0% - in other words, a tripling of the number of farm operator estates subject to federal estate tax. The report states, “total federal estate taxes for farm estates would be expected to more than double to $1.2 billion if the [current federal estate exemptions] were allowed to expire.” See the report here.

It would seem to make sense that if the federal estate tax exemption is cut in half, it would subject more farm operators to the estate tax. However, during the same period, farm estates have been growing significantly in value largely due to the increase in the value of farmland as well as pandemic-era programs that allowed many farm operations to pay down debt and increase equity. All of this is occurring amidst the larger demographic trend of farmers just simply getting older, living longer, and delaying transfers to the next generation.

Estate Tax Example

Take for example, a (very) simplified balance sheet for a married farm couple with no debt:

| 1,000 acres farmland at $10,000/acre: | $10,000,000.00 |

| Machinery and equipment | $1,500,000.00 |

| 1,200 cows | $1,800,000.00 |

| Life insurance death benefits | $1,000,000.00 |

| Savings and investments | $500,000.00 |

| TOTAL | $14,800,000.00 |

Under today’s federal estate tax laws, this couple is below the exemption limit. Assuming they died under the current limits, utilized portability and/or credit shelter trusts, and made no other taxable gifts during their lifetime, they would not have a federal estate tax concern.

Now, consider the same couple under the projected exemption limits in 2026:

Steps to Take Now

The above example outlines how dramatically different the overall estate tax on a farm operator’s estate can be based on the exemption limits when a person dies, whether portability was properly elected, whether credit shelter trusts and other estate planning instruments are utilized, and whether a person has made taxable gifts during their lifetime.

Exemption Limits When a Person Dies. We, of course, cannot predict when a person dies and what the estate tax exemption will be at that time. We can, however, plan based on what we know today and what is available to us today. What we know right now is that a married couple can pass over $27 million of assets without paying gift or estate tax. We also know that estates for married couples that are estimated to be between approximately $13.96 million and $27 million are not currently subject to federal estate tax, but may be in the future (for individuals, the range would be $6.98 million to $13.61 million). We are currently exploring, designing, and implementing strategies for our clients to utilize the estate and gift tax laws that exist today through lifetime gifting and irrevocable trust planning. It is also important to remember that a person cannot gift out of their “bonus” exemption amount first – they must gift from their “permanent” exemption amount first before they can even access the higher exemption limits. It is critical that farm families and other high net worth individuals work with an estate planning attorney that is intimately familiar with the tools and strategies that allow them to work within the existing federal estate tax framework and understand the order in which the exemption is used.

Portability. Portability allows a surviving spouse to elect to keep and “port over” their deceased spouse’s unused federal exemption limit. For example, if Spouse 1 dies with approximately $7 million of assets which all went to Spouse 2, Spouse 1 has not used any of his federal exemption limit (marital deductions are unlimited). Spouse 2 can then elect portability on a timely filed federal estate tax return and keep her deceased spouse’s $7 million exemption, which will be in addition to her own! This means that Spouse 2 will then have $14 million of federal estate tax exemption in her own name. If the federal estate tax exemption is cut in half in 2026, she will still get to keep the $7 million of unused exemption from her deceased spouse in addition to the project $6.98 million individual exemption. This means that estate planning attorneys should be actively recommending that their clients file timely federal estate tax returns and ensure the portability election is made. The highest estate tax example above assumes that no portability election was made – a huge difference in the amount of projected estate tax. The attorneys at Wagner Oehler, Ltd. prepare and file estate tax returns with portability elections to protect this incredibly valuable, time-limited exemption.

Credit Shelter Trusts. In addition to portability, in the same example above, Spouse 1 could have established an estate plan that includes a credit shelter trust. What this means is that the assets would not pass to Spouse 2. Instead, the assets would pass to a credit shelter trust for the benefit of Spouse 2. Spouse 1 would use the federal exemption limit available to him and apply it against the $7 million of assets going to the credit shelter trust. In that way, the assets are not added on to Spouse 2’s estate. Spouse 2 can still file a portability election for the remaining unused amount. This is a common estate planning strategy that all farm and high net worth estate planning attorneys should understand how to implement and design. The attorneys at Wagner Oehler, Ltd. prepare these types of estate plans every day.

Conclusion

The current federal exemption limits should not be assumed to be permanent. To the contrary, estate planning attorneys and our clients should be making plans for a decreased exemption limit and project how that will impact clients’ estates. Farm, business, and high net worth individuals should take care to work with an estate planning firm that is knowledgeable in strategies that allow clients to utilize the current exemption limits and can clearly delineate how lifetime gifts and the death of a spouse interact with the federal estate tax law. The attorneys at Wagner Oehler, Ltd. are focused on working with families and individuals that embrace this type of planning.

Interested in learning more? Contact us here. Subscribe to our YouTube channel, follow us on Facebook or sign up for our quarterly newsletter.

© 2026 Wagner Oehler, Ltd

Legal Disclaimer | Privacy Policy

Law Firm Website Design by The Modern Firm